Strategy Design Patterns¶

AlphaForge is a development and validation platform built for users to grow their own strategies. The distributed binary ships a curated set of 7 strategies (4 basic + 1 range + 2 advanced-indicator references), and this page is a collection of design patterns for assembling your own strategy JSON on top of them.

How to read this page

- The IDs of the 7 built-in strategies are listed in the CLI reference: alpha-forge strategy.

- The JSON examples on this page are written as templates for building your own custom strategy; the

strategy_idvalues use placeholdermy_*names. Replace them with meaningful names of your own and register viaalpha-forge strategy save. - Backtest result numbers are illustrative. Actual values depend on data and environment (fetch period, provider, settings).

Three design patterns on this page¶

| Pattern | Strategy type | Key indicators | Learning focus |

|---|---|---|---|

| HMM × BB × RSI | Regime-adaptive mean reversion | HMM / BBANDS / RSI | HMM regime detection + intermediate variables design |

| Regime switching | Per-regime strategy switching | HMM / SUPERTREND / BBANDS / RSI | Switching entry / exit / risk per regime via regime_config |

| Multi-timeframe | Higher-TF trend × daily entry | Weekly SMA / RSI / ATR | MTF confluence with indicators[].timeframe |

These go one step beyond the built-in hmm_bb_pipeline_v1 (HMM example) and donchian_turtle_v1 (classic Turtle trend follower) shipped with the binary, and serve as design guidance when you "start from the 7 built-ins and customize."

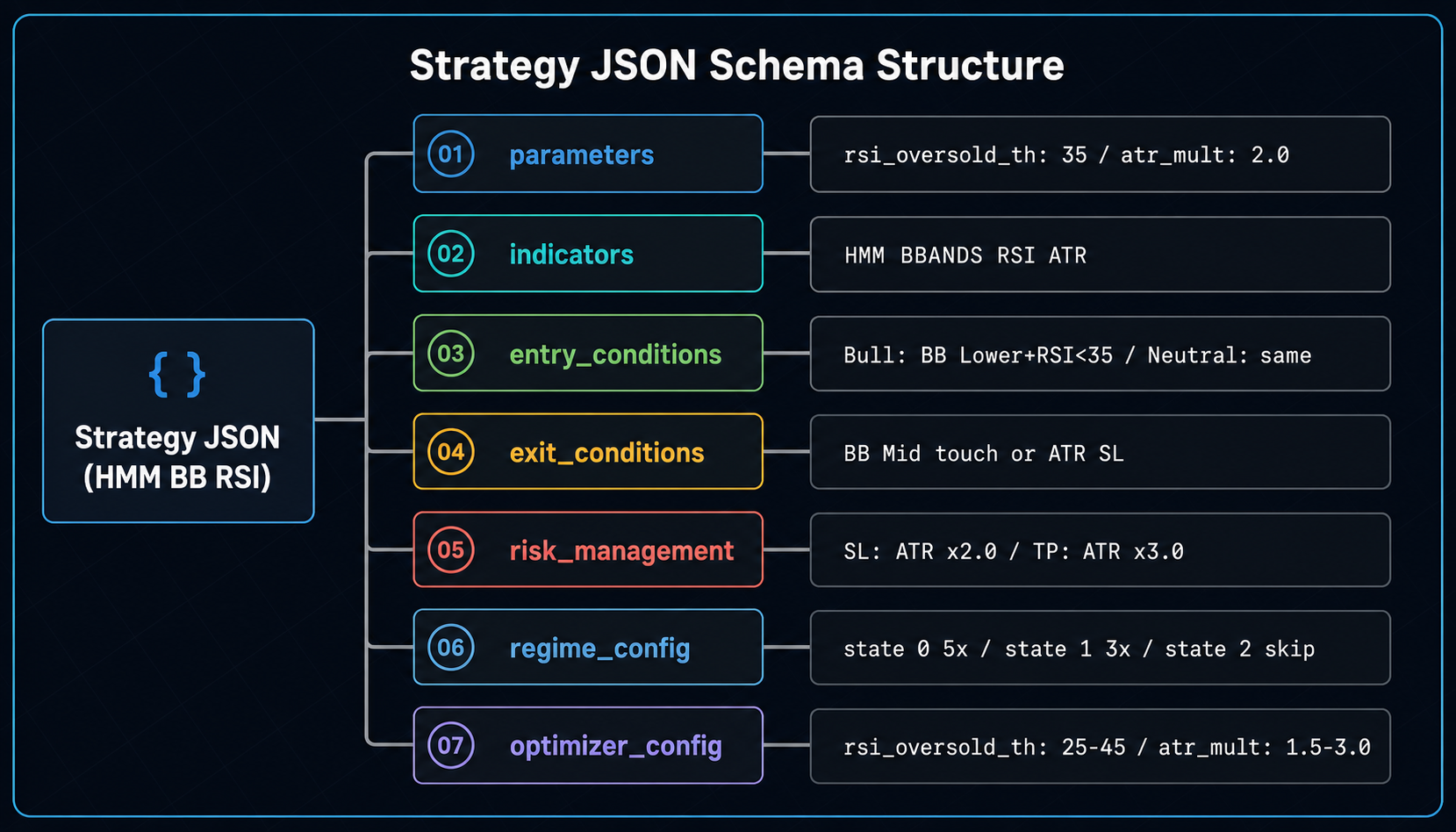

Strategy JSON basics¶

Every strategy follows the same Pydantic schema. Indicator details are available via alpha-forge analyze indicator list.

{

"strategy_id": "...",

"name": "...",

"target_symbols": [...],

"asset_type": "stock",

"timeframe": "1d",

"parameters": {...}, // Top-level parameters subject to optimization

"indicators": [...], // Computed indicators (30+ types)

"variables": [...], // Intermediate boolean variables (optional)

"entry_conditions": {...}, // Entry conditions

"exit_conditions": {...}, // Exit conditions

"risk_management": {...}, // Position size, SL/TP

"regime_config": {...}, // Regime adaptation (optional)

"optimizer_config": {...} // Optimization parameter ranges

}

About schema_version (schema generation, issue #1175)

A strategy JSON may carry an integer schema_version that denotes the schema generation for product management (distinct from the free-form user version field). It is checked on load, and JSON with a schema_version newer than the current CLI is rejected with an explicit error, prompting you to update the CLI. Older versions or no version at all (including existing JSON without a schema_version key) are read with backward compatibility, so you do not need to add it manually.

Key concepts:

indicators[].lock_on_entry: true— Freeze the value at the entry bar (used for SL/TP prices)indicators[].timeframe: "1w"— Pull values from a higher timeframe (multi-timeframe)EXPRindicator — Arbitrary pandas expression (e.g.,"close * 0.98")HMMindicator — Hidden Markov Model regime detectionregime_config— Switchentry/exit/risk_overrideper regime, keyed on the HMM output

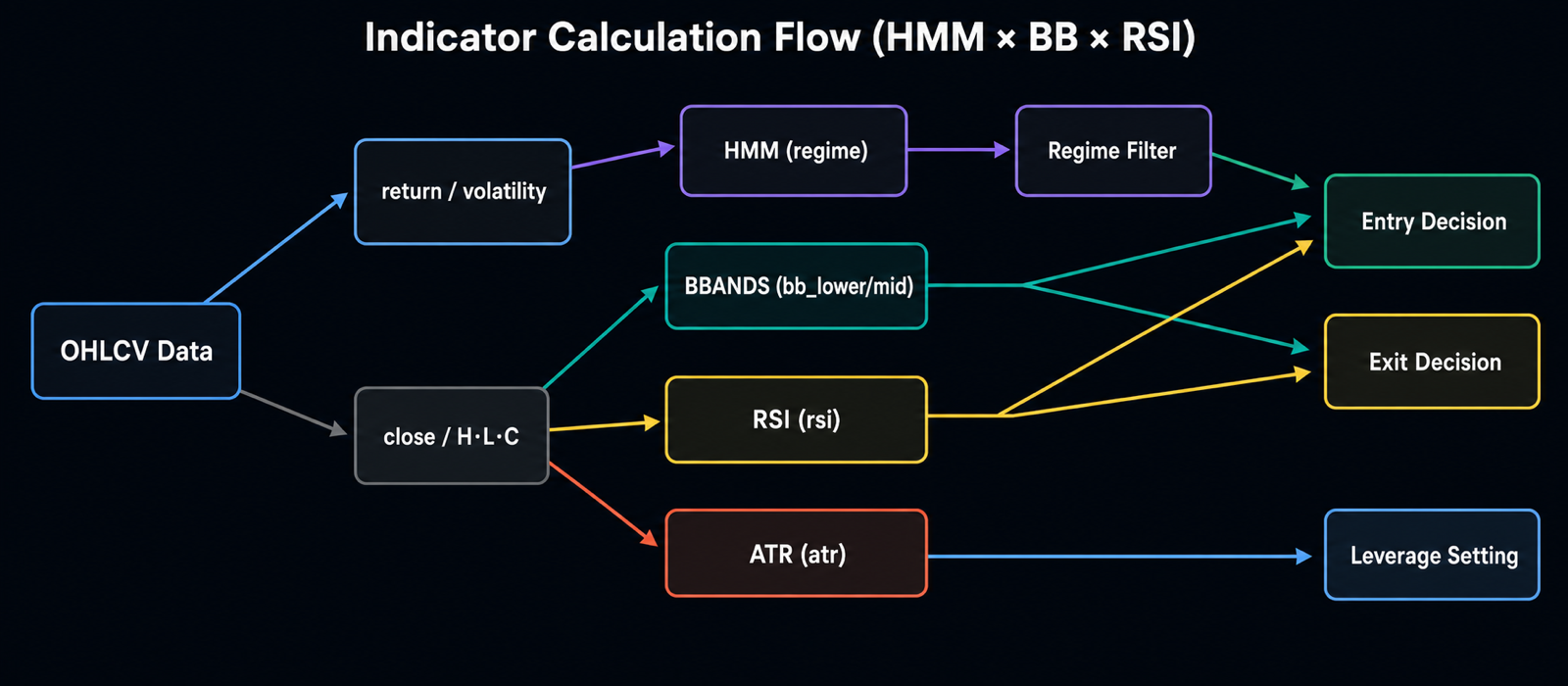

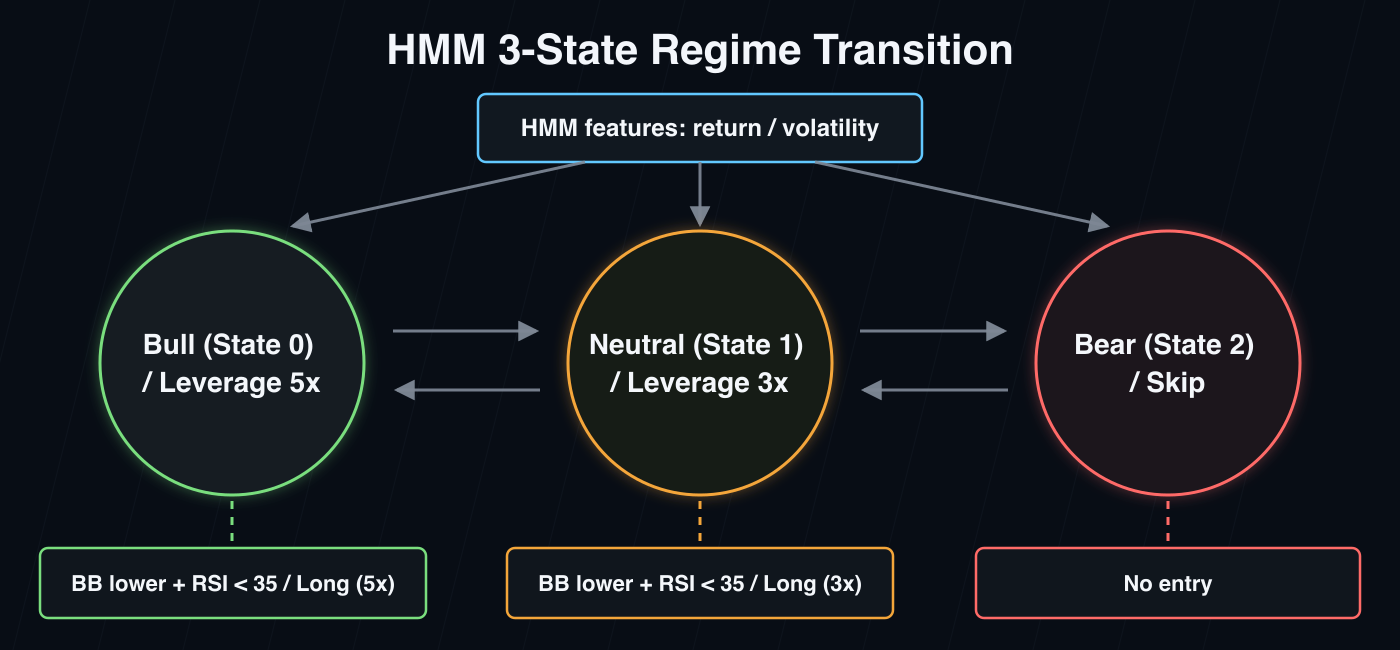

HMM × BB × RSI¶

Overview¶

Mean-reversion entries triggered by Bollinger Band lower break + RSI oversold, filtered through a 3-state HMM regime detector. Bull/Neutral/Bear regimes are distinguished, with aggressive leverage in Bull (5x), conservative in Neutral (3x), and skip in Bear.

The strength of this template is managing three regimes within a single strategy JSON. A mean-reversion strategy that works in range markets is automatically muted (or fully paused) when trends are too strong or too weak — keeping drawdowns under control.

Suitable scenarios¶

- Symbols: US large-cap ETFs (QQQ, SPY), growth stocks (NVDA), instruments with low long-horizon transaction costs

- Market environment: Mid-to-long-term regimes alternating between trend and range (like 2018-2025)

- Holding period: Days to ~2 weeks

- Risk profile: Leverage-friendly (up to 5x); HMM mis-detection can amplify drawdowns

Strategy JSON (full)¶

{

"strategy_id": "my_hmm_bb_rsi_v1",

"name": "Multi-Asset HMM×BB+RSI v1 (QQQ)",

"version": "1.0.0",

"description": "HMM 3-state regime filter × BB+RSI mean reversion. Bull(state=0): long on BB-lower + RSI oversold (leverage=5). Neutral(state=1): same condition (leverage=3). Bear(state=2): skip. Daily.",

"target_symbols": ["QQQ"],

"asset_type": "stock",

"timeframe": "1d",

"parameters": {

"rsi_oversold_th": 35,

"atr_mult": 2.0

},

"indicators": [

{ "id": "regime", "type": "HMM", "params": { "n_components": 3, "features": ["return", "volatility"] } },

{ "id": "bb_lower", "type": "BBANDS", "params": { "length": 20, "std": 2.0, "line": "lower" } },

{ "id": "bb_mid", "type": "BBANDS", "params": { "length": 20, "std": 2.0, "line": "mid" } },

{ "id": "rsi", "type": "RSI", "params": { "length": 7 } },

{ "id": "atr", "type": "ATR", "params": { "length": 14 } },

{ "id": "sl_dist", "type": "EXPR", "params": { "expr": "atr * atr_mult" }, "lock_on_entry": true }

],

"variables": [],

"entry_conditions": { "long": { "logic": "AND", "conditions": [] } },

"exit_conditions": { "long": { "logic": "OR", "conditions": [] } },

"risk_management": {

"leverage": 5.0,

"position_sizing_method": "fixed",

"position_size_pct": 100.0,

"stop_loss_indicator": "sl_dist",

"max_positions": 1

},

"regime_config": {

"indicator_id": "regime",

"default_action": "skip",

"states": {

"0": {

"entry_conditions": { "long": { "logic": "AND", "conditions": [

{ "left": "close", "op": "<", "right": "bb_lower" },

{ "left": "rsi", "op": "<", "right": "rsi_oversold_th" }

]}},

"exit_conditions": { "long": { "logic": "OR", "conditions": [

{ "left": "close", "op": ">", "right": "bb_mid" }

]}},

"risk_override": { "leverage": 5.0, "position_sizing_method": "fixed", "position_size_pct": 100.0 }

},

"1": {

"entry_conditions": { "long": { "logic": "AND", "conditions": [

{ "left": "close", "op": "<", "right": "bb_lower" },

{ "left": "rsi", "op": "<", "right": "rsi_oversold_th" }

]}},

"exit_conditions": { "long": { "logic": "OR", "conditions": [

{ "left": "close", "op": ">", "right": "bb_mid" }

]}},

"risk_override": { "leverage": 3.0, "position_sizing_method": "fixed", "position_size_pct": 100.0 }

},

"2": {}

}

},

"backtest_config": {

"regime_analysis": {

"method": "hmm",

"hmm_indicator_id": "regime",

"label_names": { "0": "Bull", "1": "Neutral", "2": "Bear" }

}

},

"optimizer_config": {

"param_ranges": {

"bb_lower.length": { "min": 15, "max": 25, "step": 1 },

"bb_lower.std": { "min": 1.8, "max": 2.5, "step": 0.1 },

"rsi.length": { "min": 5, "max": 14, "step": 1 },

"rsi_oversold_th": { "min": 25, "max": 45, "step": 5 },

"atr_mult": { "min": 1.5, "max": 3.0, "step": 0.5 }

},

"constraints": { "min_trades": 20 },

"metric": "sharpe_ratio"

},

"tags": ["hmm", "bb", "rsi", "mean-reversion", "leverage", "nas100"]

}

Key parameters¶

| Parameter | Role | Recommended range |

|---|---|---|

regime.n_components |

HMM state count | 3 (Bull/Neutral/Bear) |

regime.features |

HMM input features | ["return", "volatility"] |

bb_lower.length / std |

BB period and std multiplier | period 15-25, std 1.8-2.5 |

rsi.length |

RSI period | 5-14 (shorter = more responsive) |

rsi_oversold_th |

Entry threshold | 25-45 (lower = stricter) |

atr_mult |

ATR-based SL multiplier | 1.5-3.0 |

risk_override.leverage |

Per-regime leverage | Bull 5.0 / Neutral 3.0 / Bear 0 (skip) |

Sample backtest output¶

Sample output

Numbers depend on data and environment.

==> QQQ 2018-01-01 → 2025-12-31 (1d)

trades: 38 win_rate: 65.8% profit_factor: 2.15

total_return: +124.5% cagr: +10.7% sharpe: 1.42

max_drawdown: -18.4% exposure: 24.3%

final_equity: $22,450 (initial: $10,000)

Customization tips¶

- Change the symbol: Replace

target_symbolswith["SPY"],["NVDA"],["GC=F"], etc. - Change state count:

regime.n_components: 2(Bull/Bear) simplifies the decision;4adds nuance (requires more data) - Strengthen entry: Add

volume > sma_volume_20or similar conditions inregime_config.states["0"].entry_conditions - Optimize:

alpha-forge optimize run QQQ --strategy my_hmm_bb_rsi_v1 --metric sharpe_ratio --save

Regime switching¶

Overview¶

A pattern that applies different strategies per regime, keyed on HMM output. Within a single strategy JSON, the Bull regime runs trend-following and the Bear/Range regime runs mean reversion — swapping the strategy itself rather than just parameters.

The defining feature versus HMM × BB × RSI: regime_config.states lets you define entry_conditions and exit_conditions completely independently per regime.

Suitable scenarios¶

- Symbols: Commodity futures (CL=F, GC=F, NG=F) — high-volatility instruments with clear trend/range alternation

- Market environment: Capture both trend and counter-trend behavior typical of commodity markets

- Holding period: Days to a month

- Risk profile: High leverage (10x) + ATR-based SL; assumes margin-based commodity trading

Strategy JSON (full)¶

{

"strategy_id": "my_regime_switching_v1",

"name": "Commodity HMM Regime v1",

"version": "1.0.0",

"description": "Regime-adaptive for commodity CFDs: HMM 2-state Bull/Bear. Bull = SuperTrend long, Bear = BB+RSI mean reversion. leverage=10.",

"target_symbols": ["GC=F", "SI=F", "CL=F", "BZ=F", "NG=F", "ZC=F", "ZS=F", "ZW=F", "HG=F"],

"asset_type": "stock",

"timeframe": "1d",

"parameters": {

"adx_threshold": 20,

"rsi_threshold": 35,

"atr_mult": 2.0

},

"indicators": [

{ "id": "regime", "type": "HMM", "params": { "n_components": 2, "features": ["return", "volatility"], "volatility_window": 10 } },

{ "id": "supertrend_val", "type": "SUPERTREND", "params": { "length": 9, "multiplier": 3.0 } },

{ "id": "adx_val", "type": "ADX", "params": { "length": 14 } },

{ "id": "bb_lower", "type": "BBANDS", "params": { "length": 20, "std": 2.0, "line": "lower" } },

{ "id": "bb_mid", "type": "BBANDS", "params": { "length": 20, "std": 2.0, "line": "mid" } },

{ "id": "rsi", "type": "RSI", "params": { "length": 14 } },

{ "id": "atr", "type": "ATR", "params": { "length": 14 } },

{ "id": "sl_dist", "type": "EXPR", "params": { "expr": "atr * atr_mult" }, "lock_on_entry": true }

],

"variables": [],

"entry_conditions": { "long": { "logic": "AND", "conditions": [] } },

"exit_conditions": { "long": { "logic": "OR", "conditions": [] } },

"risk_management": {

"leverage": 10.0,

"position_sizing_method": "risk_based",

"risk_per_trade_pct": 1.5,

"stop_loss_indicator": "sl_dist",

"max_positions": 1

},

"regime_config": {

"indicator_id": "regime",

"states": {

"0": {

"entry_conditions": { "long": { "logic": "AND", "conditions": [

{ "left": "close", "op": "crosses_above", "right": "supertrend_val" },

{ "left": "adx_val", "op": ">", "right": "adx_threshold" }

]}},

"exit_conditions": { "long": { "logic": "OR", "conditions": [

{ "left": "close", "op": "crosses_below", "right": "supertrend_val" }

]}}

},

"1": {

"entry_conditions": { "long": { "logic": "AND", "conditions": [

{ "left": "close", "op": "<", "right": "bb_lower" },

{ "left": "rsi", "op": "<", "right": "rsi_threshold" }

]}},

"exit_conditions": { "long": { "logic": "OR", "conditions": [

{ "left": "close", "op": ">", "right": "bb_mid" }

]}}

}

}

},

"backtest_config": {

"regime_analysis": {

"method": "hmm",

"hmm_indicator_id": "regime",

"label_names": { "0": "Bull", "1": "Bear" }

}

},

"optimizer_config": {

"param_ranges": {

"supertrend_val.multiplier": { "min": 2.0, "max": 4.0, "step": 0.5 },

"adx_threshold": { "min": 15, "max": 30, "step": 5 },

"rsi_threshold": { "min": 25, "max": 45, "step": 5 },

"atr_mult": { "min": 1.5, "max": 3.0, "step": 0.5 }

},

"constraints": { "min_trades": 15 },

"metric": "sharpe_ratio"

},

"tags": ["hmm", "regime", "adaptive", "commodity", "leverage-10"]

}

Key parameters¶

| Parameter | Role | Recommended range |

|---|---|---|

regime.n_components |

HMM state count | 2 (simple Bull/Bear switch) |

regime.volatility_window |

Volatility computation window | 10 (short) to 30 (mid) |

supertrend_val.multiplier |

SuperTrend channel width | 2.0-4.0 (smaller = more responsive) |

adx_threshold |

Trend strength threshold | 15-30 (≥25 = strong trend) |

rsi_threshold |

Mean-reversion oversold threshold | 25-45 |

risk_per_trade_pct |

% risk per trade | 1.5 (conservative) |

leverage |

Commodity futures leverage | 10 (margin trading assumed) |

Sample backtest output¶

Sample output

==> CL=F 2018-01-01 → 2025-12-31 (1d)

trades: 27 win_rate: 51.9% profit_factor: 1.82

total_return: +88.3% cagr: +8.4% sharpe: 1.21

max_drawdown: -22.1% exposure: 31.5%

Running a strategy that sets backtest_config.regime_analysis with --regime adds a per-regime performance block (numbers are illustrative):

=== Per-Regime Performance ===

Bull : Trades= 14 | Sharpe= 1.45 | WinRate= 57.1% | MDD= 12.30%

Bear : Trades= 13 | Sharpe= 0.92 | WinRate= 46.2% | MDD= 22.10%

Output structure

With --json, the regime_breakdown key is returned as { "method", "description", "periods": [...], "aggregates": {...} }. Each entry in periods holds fields such as label / start / end / sharpe / total_trades for a contiguous regime segment, and aggregates holds per-label averages (such as sharpe_avg).

Customization tips¶

- Add more states:

n_components: 3for Bull/Range/Bear; addstates["2"] - Switch to equities: Replace

target_symbolswith stocks and lowerrisk_management.leverageto1.0-2.0 - More entries: Loosen each regime's

entry_conditions(e.g.,adx_threshold: 15,rsi_threshold: 45) - Cross-symbol optimize:

alpha-forge optimize cross-symbol GC=F SI=F CL=F --strategy my_regime_switching_v1 --aggregation min --save

Multi-timeframe¶

Overview¶

Use the indicators[].timeframe field to pull higher-timeframe values while entering on the lower timeframe. Judge a long-term trend on the weekly SMA and time pullback entries on the daily RSI.

Educational example

The strategy JSON in this section is written as an example of the indicators[].timeframe feature. Validate behavior with alpha-forge strategy validate and alpha-forge backtest run before live use.

Suitable scenarios¶

- Symbols: US large-cap stocks / ETFs (SPY, QQQ, AAPL)

- Market environment: Long-term uptrend with short-term pullbacks

- Holding period: 1 day to 2 weeks

- Risk profile: Trend-following design — watch for drawdowns at trend reversals. Skips entries entirely when the weekly trend turns down.

Strategy JSON (full)¶

{

"strategy_id": "my_mtf_pullback_v1",

"name": "SPY Multi-Timeframe Trend Pullback v1",

"version": "1.0.0",

"description": "Multi-timeframe strategy: judge trend with weekly SMA, time pullback entries on daily RSI oversold.",

"target_symbols": ["SPY"],

"asset_type": "stock",

"timeframe": "1d",

"parameters": {

"rsi_oversold_th": 35,

"atr_mult": 2.0

},

"indicators": [

{

"id": "weekly_sma",

"type": "SMA",

"params": { "length": 20 },

"source": "close",

"timeframe": "1w"

},

{

"id": "weekly_close",

"type": "EXPR",

"params": { "expr": "close" },

"timeframe": "1w"

},

{ "id": "rsi", "type": "RSI", "params": { "length": 7 } },

{ "id": "sma_50", "type": "SMA", "params": { "length": 50 } },

{ "id": "atr", "type": "ATR", "params": { "length": 14 } },

{ "id": "sl_dist", "type": "EXPR", "params": { "expr": "atr * atr_mult" }, "lock_on_entry": true }

],

"variables": [

{

"id": "weekly_uptrend",

"logic": "AND",

"conditions": [

{ "left": "weekly_close", "op": ">", "right": "weekly_sma" }

]

}

],

"entry_conditions": {

"long": {

"logic": "AND",

"conditions": [

{ "left": "weekly_uptrend", "op": "==", "right": true },

{ "left": "close", "op": ">", "right": "sma_50" },

{ "left": "rsi", "op": "<", "right": "rsi_oversold_th" }

]

}

},

"exit_conditions": {

"long": {

"logic": "OR",

"conditions": [

{ "left": "rsi", "op": ">", "right": 60 },

{ "left": "close", "op": "<", "right": "sma_50" }

]

}

},

"risk_management": {

"leverage": 1.0,

"position_sizing_method": "fixed",

"position_size_pct": 25.0,

"stop_loss_indicator": "sl_dist",

"max_positions": 1

},

"regime_config": null,

"optimizer_config": {

"param_ranges": {

"weekly_sma.length": { "min": 10, "max": 30, "step": 5 },

"rsi.length": { "min": 5, "max": 14, "step": 1 },

"rsi_oversold_th": { "min": 25, "max": 45, "step": 5 },

"atr_mult": { "min": 1.5, "max": 3.0, "step": 0.5 }

},

"constraints": { "min_trades": 20 },

"metric": "sharpe_ratio"

},

"tags": ["multi-timeframe", "trend-following", "pullback", "weekly", "spy"]

}

Key parameters¶

| Parameter | Role | Recommended range |

|---|---|---|

weekly_sma.timeframe: "1w" |

Higher timeframe for the SMA | "1w" (also "4h", "1mo") |

weekly_sma.length |

Weekly SMA period | 10-30 (mid-to-long trend) |

rsi.length |

Daily RSI period | 5-14 |

rsi_oversold_th |

Pullback threshold | 25-45 |

sma_50 |

Daily mid-trend filter | fixed 50 |

position_size_pct |

Per-position size | 25% (conservative) |

The indicators[].timeframe field computes only that indicator on a different timeframe. When a daily-base strategy (timeframe: "1d") references a weekly indicator, the matching weekly value is automatically forward-filled (ffill) to align with each daily row.

Sample backtest output¶

Sample output

==> SPY 2018-01-01 → 2025-12-31 (1d)

trades: 32 win_rate: 62.5% profit_factor: 1.95

total_return: +68.2% cagr: +6.7% sharpe: 1.18

max_drawdown: -14.3% exposure: 28.7%

Customization tips¶

- Change the higher timeframe:

weekly_sma.timeframe: "4h"for intraday MTF;"1mo"for monthly-led strategies - Combine multiple higher timeframes: Require both weekly and monthly SMAs to be cleared before entering

- Expand symbols:

target_symbols: ["SPY", "QQQ", "DIA"]and usealpha-forge optimize cross-symbolfor robust parameters - Add shorts: Define

entry_conditions.shortfor "weekly downtrend + daily RSI overbought"

Customization and derivations¶

Parameter optimization¶

Each template includes optimizer_config.param_ranges, so Optuna Bayesian optimization runs with:

See alpha-forge optimize run for details.

Walk-forward to guard against overfitting¶

Each window runs IS optimization → OOS evaluation; check overfitting_score afterwards.

Sensitivity analysis to measure robustness¶

Sweep around optimized parameters and measure how much the metric moves. If overall_robustness_score ≤ 0.7, suspect overfitting.

Compare with live results¶

Once trade records accumulate, compare against backtest:

Related documentation¶

- Getting Started — Start with a simple SMA crossover

- CLI Reference — All

alpha-forgecommand parameters - AI-Driven Strategy Exploration Workflow — Generate strategies with Claude Code / Codex